Operating Costs

- Rent: The cost of renting an office or warehouse, including upkeep costs for the business space.

- Utilities: Costs associated with running a business, such as internet, water, and power.

- Salaries and Wages: Payments made to workers, such as bonuses and other incentives.

- Employee Training: Expenses related to enhancing workers’ skills to boost productivity.

- Supplies: The price of buying goods or resources that are used directly in business operations.

Interest Expenses

The UAE corporate tax law enables interest to be deducted from taxable earnings, but it is liable to certain limitations. There are particular regulations for interest deductions to avoid base erosion and profit shifting (BEPS) via excessive debt financing.

Expenses for deductible interest could include:

- Business loan interest

- Interest paid on business-related credit lines or overdrafts

- Finance fees for financial leases

- The interest part of Islamic finance plans

It’s important to remember, though, that the general and particular interest restriction rules determine whether or not interest is deductible.

Charitable Contributions

The CT Law defines that only contributions to qualifying public benefit organizations are deductible, making sure only donations serving the public good and related to the company’s objective are considered for tax relief.

Entertainment Expenditure

Only 50% of the expenses can be deducted for entertainment expenses, such as lunches or gatherings for clients or business associates.

For example, if a business spends AED 100,000 on entertaining customers, only AED 50,000 is tax-deductible. However, if the cost is for staff amusement (e.g., a company party), it can be fully tax-deductible, unless the event is personal in nature (e.g., a wedding ceremony).

Depreciation of Assets

Companies can deduct depreciation costs for fixed assets like vehicles, machinery, and office supplies based on prescribed accounting methods.

Marketing and Advertising Costs

Expenses related to branding, marketing, and advertising expenditures are deductible if they are associated with the business.

Legal and Professional Fees

For business-related services, payments to tax advisors, consultants, auditors, and attorneys are deductible.

Conditions for Deductibility

1.Expenditure Must Be Solely for Business

For expenses to be deductible, they must be incurred exclusively for the purpose of making revenue or carrying out commercial operations. Claims cannot be made for personal costs or expenses unrelated to business operations.

2. Timing of Expenses

Expenses must be reported within the fiscal year in which they are incurred. Companies should match their accounting periods with their spending claims to prevent problems during audits.

3. Apportioning Mixed Expenditures

Businesses must divide expenses if they are partially for non-business and partially for company use. The only part that is deductible is the part that is directly tied to producing taxable income.

Example: If a company pays office rent and uses a portion of the space for personal use, only the portion that is relevant to business operations is deductible.

4. Expenses Must Not Be Capital in Nature

Capital expenditures cannot be deducted from expenses. Typically, capital expenditures entail sizable investments in assets that yield long-term gains (e.g., purchasing property or machinery). Rather, the operating costs incurred within a fiscal year should be subject to deductible expenses.

5. Expenses Must Be Properly Documented

Supporting claims for deductible expenses requires accurate documentation. Companies should keep:

- Invoices and receipts that identify the nature of the expenditure.

- Documents detailing how each expenditure relates to company activities.

- Financial statements that accurately reflect these transactions with precise accounting entries.

What Are Non-Deductible Expenses?

Non-deductible expenses are business costs that cannot be subtracted from a company’s taxable income when calculating its corporate tax liability. These are essentially expenditures that companies are not permitted to deduct under UAE tax legislation, even if they are directly related to the daily activities of the company.

The primary difference of non-deductible expenses is that they are not directly related to the development of company revenue or are considered outside the boundaries of what the tax authorities consider eligible for deduction. Although businesses may incur these costs during operations, they cannot be claimed to reduce taxable income on tax returns.

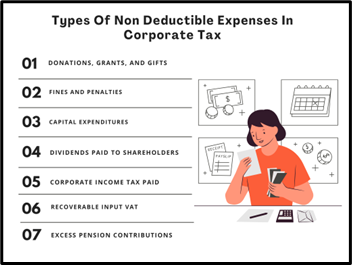

Types of nondeductible expenses in corporate tax